Futures Calls Recap for 4/18/16

A nice day for futures with two Opening Range plays that worked and also an NQ call after the Value Area set that worked big as well. The markets gapped down, filled the gap, and closed higher on 1.5 billion NASDAQ shares.

Net ticks: +37 ticks.

As usual, let's start by taking a look at the ES and NQ with our market directional lines, VWAP, and Comber on the 5-minute chart from today's session:

ES and NQ Opening and Institutional Range Plays:

ES Opening Range Play triggered long at A and worked:

NQ Opening Range Play triggered long at A and worked:

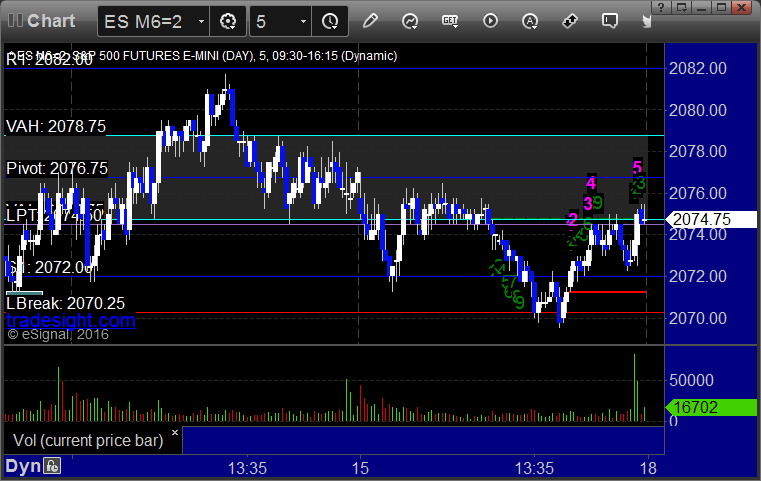

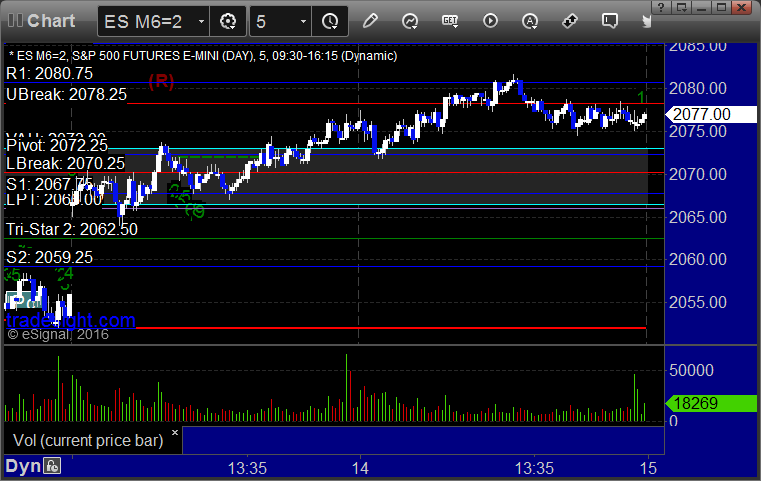

ES Tradesight Institutional Range Play:

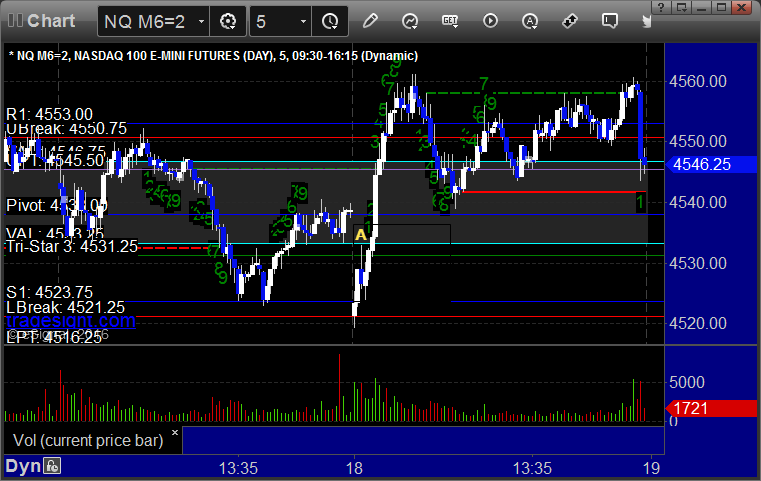

NQ Tradesight Institutional Range Play:

NQ:

Just a reminder that we use half points for ticks on the NQ and not the quarter point measurement that the exchanges switched to in recent years. This allows us to use 6 ticks as a key target as we do on the other contracts. It also keeps the value of a tick at $10, closer to the value of a tick on the other contracts.

My call triggered long at A at 4533.75, hit first target for 6 ticks and much more. Stopped out of the second half at 4550.50:

Forex Calls Recap for 4/18/16

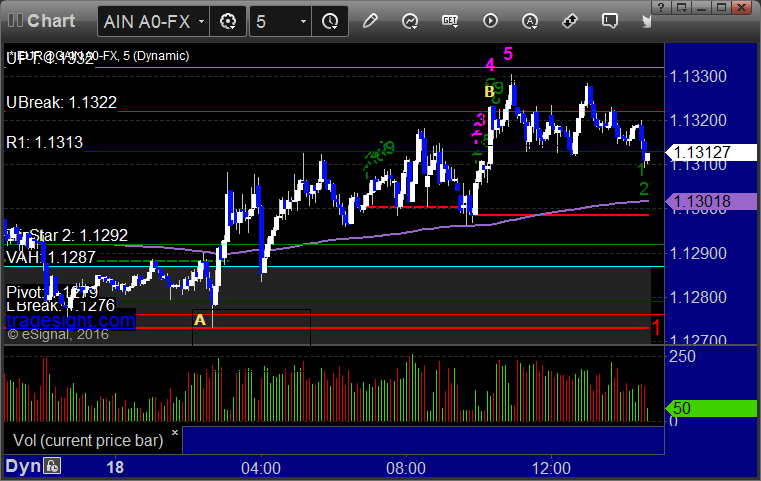

Only 60 pips of range from high to low on the EURUSD, making for a waste of a session. See that section below.

Here's a look at the US Dollar Index intraday with our market directional lines:

EURUSD:

A piece of the trade triggered short at A and stopped. Triggered long at B and never went anywhere, closed at end of day for just over 10 pip loss:

Tradesight March 2016 Stock Results

Tradesight has been providing stock calls daily since 2002. We post the results of our of our trades, winners and losers, in our reports and Market Blog every day. Some people might find it surprising to learn that while we track our Futures and Forex formal trade call results monthly, we don’t post anything beyond the trade reviews on our Stocks calls.

There is actually a very specific reason for this. I’ve never been a fan of trying to “hype” or “promote” something. Being profitable in trading is about learning what to do and getting yourself to make the right decisions. In Futures as well as in Forex, if we publish a call in advance, just about everyone should get the same fills and be able to get in and out at almost the same numbers. That isn’t always the case in stocks. It depends on how many shares you are trading and what the liquidity in the market for that stock is at the time. For that reason, I have already been hesitant to say “These are the exact results.” I would never want to try to suggest that someone would make a certain amount of dollars trading a certain number of shares or make a certain percentage. If I take a trade and sell it for a $0.30 gain, it makes a big statistical difference if someone else had to pay $0.05 more to get in and maybe got out for $0.02 less. That’s $0.23 instead of $0.30 even though the concept of the trade was fine.

However, after many requests, in October 2015, we started posting our results. You can see these monthlyhere.

In our system, you can basically break trades down into four categories: Big losers, small losers, small winners, and big winners.

In order to have any chance of succeeding in the markets, you have to have a system. There is no other way around it. I’ve been trading for 20 years now, and I’ve trained over 1000 people. You don’t make money if you don’t have a technically valid system for entry and exits.

Of the four categories of trades listed above, we simply don’t allow any of the first category, which is big losers. We always have a worst-case stop and we always stick to it. There should never be a scenario where you are still in a trade that is causing a significant loss if you follow our rules.

In terms of the other three categories, generally speaking, if you have about a third of your trades fall into each category, you should be making good money. In other words, if we have about 33% of our trades as small losers and 33% of trades as small winners, those basically would offset. That leaves the other 33% of so only as bigger winners, and that’s what we are here for. In our world, we count a loser as a trade that stops out (stops in our system are based on the price-level of the stock). We count a small winner as a trade that goes enough to make a partial and then either stops the second half of the trade under the entry or stops the second half of the trade slightly in the money, but no more than the partial was or so. Then the big winners are anything that keeps going beyond the partial.

So these were the results for February.

Tradesight Stock Results for February 2016

Number of trade calls that triggered with market support: 132

Number (and percent of total) of small losers: 26 (19.7%)

Number (and percent of total) of small winners: 48 (36.3%)

Number (and percent of total) of big winners: 58 (44%)

And for March?

Tradesight Stock Results for March 2016

Number of trade calls that triggered with market support: 102

Number (and percent of total) of small losers: 32 (28.4%)

Number (and percent of total) of small winners: 30 (29.4%)

Number (and percent of total) of big winners: 43 (42.2%)

The overall win rate is 71.6%, still holding up well. We saw about 30 less trades trigger in March, mostly due to the fact that market volume slowed down quite a bit from January and February. Still, these numbers remain remarkably close to the 33/33/33 split we like to see, and there were quite a few huge winners over the course of the month that should have paid the bills.

Tradesight March 2016 Futures Results

Before we get to March’s numbers, here is a short reminder of the results from February. The full report from February can be found here. You can also go back indefinitely by clicking here and scrolling down.

Tradesight Tick Results for February 2016

Number of trades: 58

Number of losers: 18

Winning percentage: 69%

Net ticks: +145 ticks

Reminder: Here are the rules.

1) Totals for the month are based on trades that occurred on trading days in the calendar month.

2) Trades are based on the calls in the Twitter feed exactly as we call them and manage them as well as the Opening Range plays under the basic strategy we teach for those in our course. We do not count everything you could have done from taking our courses and using our tools.

3) All trades are broken into two pieces, with the assumption that one half is sold at the first target and one half is sold at the final exit. These are then averaged. So if we made 6 ticks on one half and 12 on the second, that’s a 9-tick winner.

4) Pure losers (trades that just stop out) are considered 7 tick losers. We don’t risk more than that in the Twitter calls.

It is important to note that these results do not include the Tradesight Value Area or Institutional Range plays, all of which have been working quite well on their own.

You can go through the reports and compare the breakdown that I give as each trade is reviewed.

Tradesight Tick Results for March 2016

Number of trades: 60

Number of losers: 18

Winning percentage: 70%

Net ticks: +60.5 ticks

March wasn't as nice in the market as the prior months, largely because volume dropped off quite a bit out of the blue from what we saw to start the year. Still, our Opening Range plays continue to work about 80% of the days, and even with a few less other trades to call, we booked gains for the month and a great winning ratio. Also, we typically shouldn't trade on the day of quarterly contract roll, but the Opening Range plays there (since I didn't call them off) cost 26 ticks alone.

Tradesight March 2016 Forex Results

Before we get to March’s numbers, here is a short reminder of the results from February. The full report from February can be found here and you can get the last several months in a row vertically by clicking here and scrolling down.

Tradesight Pip Results for February 2016

Number of trades: 31

Number of losers: 15

Winning percentage: 51.6%

Worst losing streak: 5 in a row

Net pips: +195 pips

Reminder: Here are the rules.

1) Calls made in the calendar month count. In other words, a call made on August 31 that triggered the morning of September 1 is not part of September. Calls made on Thursday, September 30 that triggered between then and the morning of October 1 ARE part of September.

2) Trades that triggered before 8 pm EST / 5 pm PST (i.e. pre Asia) and NEVER gave you a chance to re-enter are NOT counted. Everything else is counted equally.

3) All trades are broken into two pieces, with the assumption that one half is sold at the first target and one half is sold at the final exit. These are then averaged. So if we made 40 pips on one half and 60 on the second, that’s a 50-pip winner. If we made 40 pips on one half, never adjusted our stop, and the second half stopped for the 25 pip loser, then that’s a 7 pip winner (15 divided by 2 is 7.5, and I rounded down).

4) Pure losers (trades that just stop out) are considered 25 pip losers. In some cases, this can be a few more or a few less, but it should average right in there, so instead of making it complicated, I count them as 25 pips.

5) Trade re-entries are valid if a trade stops except between 3 am EST and 9 am EST (when I’m sleeping). So in other words, even if you are awake in those hours and you could have re-entered, I’m only counting things that I would have done. This is important because otherwise the implication is that you need to be awake 24/6. Triggers that occur right on the Big Three news announcements each month don’t count as you shouldn’t have orders in that close at that time.

You can go through the reports and compare the breakdown that I give as each trade is reviewed.

Tradesight Pip Results for March 2016

Number of trades: 35

Number of losers: 14

Winning percentage: 60%

Worst losing streak: 3 in a row

Net pips: +545 pips

March turned out to be our biggest month in a while with a nice 60% win ratio and several trades that held for well over 100 pips to the final exits. Average ranges for the month stayed about...average, with the EURUSD 6 month average holding around 105 pips and the GBPUSD holding at 125. The US Dollar Index actually moved a bit, helping us maintain some day over day winners. All told, it was a nice month.

Stock Picks Recap for 4/14/16

With each stock's recap, we will include a (with market support) or (without market support) tag, designating whether the trade triggered with or without market directional support at the time. Anything in the first five minutes will be considered WITHOUT market support because market direction cannot be determined that early. ETF calls do not require market support, and are thus either winners or losers.

From the report, SPNC triggered long (without market support due to opening 5 minutes) and worked:

From the Messenger/Tradesight_st Twitter Feed, TWTR triggered long (with market support) and worked:

CELG triggered short (without market support) and worked:

In total, that's 1 trade triggering with market support, and it worked.

Futures Calls Recap for 4/14/16

The markets opened flat and gave us some Opening Range winners, but most of the day was dead with options unraveling behind us as we wait for options expiration Friday. NASDAQ volume was 1.5 billion shares.

Net ticks: +16.5 ticks.

As usual, let's start by taking a look at the ES and NQ with our market directional lines, VWAP, and Comber on the 5-minute chart from today's session:

ES and NQ Opening and Institutional Range Plays:

ES Opening Range Play triggered short at A and worked:

NQ Opening Range Play triggered short at A and worked:

ES Tradesight Institutional Range Play:

NQ Tradesight Institutional Range Play:

ES:

Forex Calls Recap for 4/14/16

Another dull session. See EURUSD section below. Really not much to discuss. A couple of 13 signals worked.

Here's a look at the US Dollar Index intraday with our market directional lines:

Stock Picks Recap for 4/15/16

With each stock's recap, we will include a (with market support) or (without market support) tag, designating whether the trade triggered with or without market directional support at the time. Anything in the first five minutes will be considered WITHOUT market support because market direction cannot be determined that early. ETF calls do not require market support, and are thus either winners or losers.

From the report, CERS triggered, but of course exactly on the wrong day for it, so we will watch Monday as it didn't move Friday with the market at all, stayed within a couple of cents:

MELI triggered long (without market support) and worked:

From the Messenger/Tradesight_st Twitter Feed, LULU triggered long (without market support) and worked:

SINA triggered short (with market support) and didn't work:

In total, that's 1 trade triggering with market support, and it didn't work but the other two did.

Futures Calls Recap for 4/15/16

Pretty much what we expected coming into the week...a dead flat morning for options expiration. What is amazing is how light volume was for an expiration...only 1.5 billion NASDAQ shares. Opening ranges worked and no additional calls.

Net ticks: +5 ticks.

As usual, let's start by taking a look at the ES and NQ with our market directional lines, VWAP, and Comber on the 5-minute chart from today's session:

ES and NQ Opening and Institutional Range Plays:

ES Opening Range Play triggered short at A and ended up working but I stopped out over the OR low because things were so dead:

NQ Opening Range Play triggered short at A and worked:

ES Tradesight Institutional Range Play:

NQ Tradesight Institutional Range Play:

ES: