Stock Picks Recap for 8/5/13

With each stock's recap, we will include a (with market support) or (without market support) tag, designating whether the trade triggered with or without market directional support at the time. Anything in the first five minutes will be considered WITHOUT market support because market direction cannot be determined that early. ETF calls do not require market support, and are thus either winners or losers.

For the first time in a long time that I can remember (except Holidays), neither the calls in the report nor the intraday calls triggered. Nothing happened. Just not enough movement in a 5-point ES range.

In total, nothing happened.

Futures Calls Recap for 8/5/13

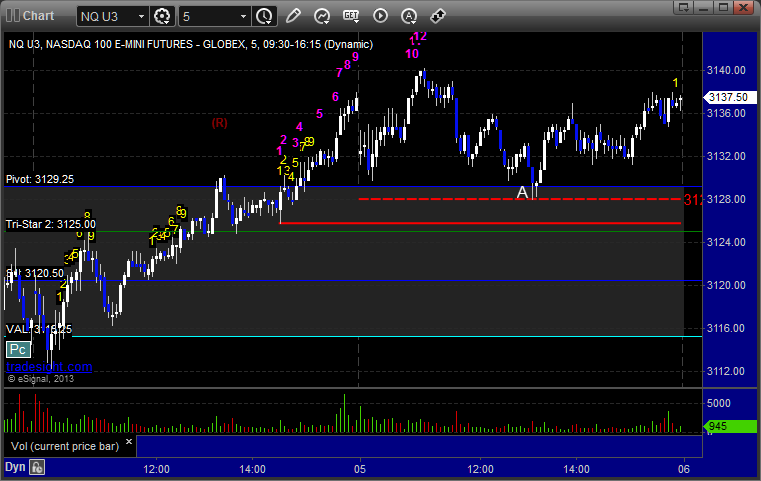

A really great setup in the NQ ended up stopping, mostly because we just suffered through one of the most inactive, light volume days of the year. NASDAQ volume closed at 1.3 billion shares, probably not helped by the global terror warning.

Net ticks: -7 ticks.

As usual, let's start by taking a look at the ES and NQ with our market directional lines, VWAP, and Comber on the 5-minute chart from today's session:

NQ:

Just a reminder that we use half points for ticks on the NQ and not the quarter point measurement that the exchanges switched to in recent years. This allows us to use 6 ticks as a key target as we do on the other contracts. It also keeps the value of a tick at $10, closer to the value of a tick on the other contracts.

Triggered short at A at 3129.00 with a great head and shoulders pattern, the Value Area, and the VAH lined up with the Pivot. About as good as they come, but when you don't have volume...it stopped:

Futures Calls Recap for 8/5/13

A really great setup in the NQ ended up stopping, mostly because we just suffered through one of the most inactive, light volume days of the year. NASDAQ volume closed at 1.3 billion shares, probably not helped by the global terror warning.

Net ticks: -7 ticks.

As usual, let's start by taking a look at the ES and NQ with our market directional lines, VWAP, and Comber on the 5-minute chart from today's session:

NQ:

Just a reminder that we use half points for ticks on the NQ and not the quarter point measurement that the exchanges switched to in recent years. This allows us to use 6 ticks as a key target as we do on the other contracts. It also keeps the value of a tick at $10, closer to the value of a tick on the other contracts.

Triggered short at A at 3129.00 with a great head and shoulders pattern, the Value Area, and the VAH lined up with the Pivot. About as good as they come, but when you don't have volume...it stopped:

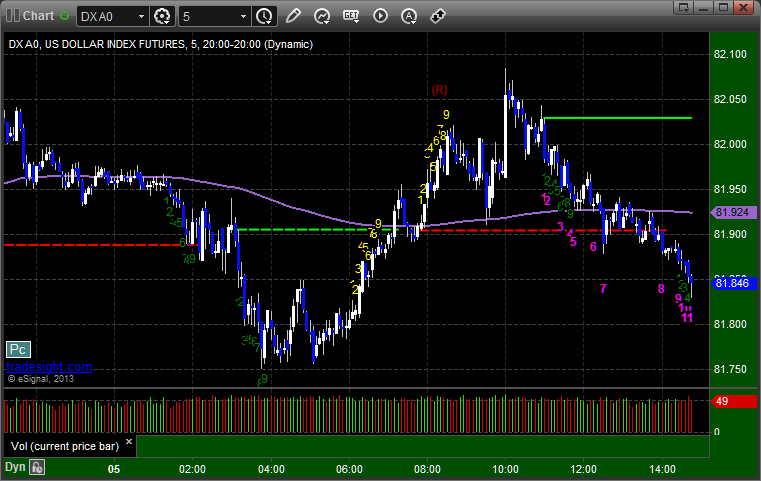

Forex Calls Recap for 8/5/13

A clean winner that made good use of the levels on the GBPUSD, and we're still holding the second half of the trade. See that section below.

Here's a look at the US Dollar Index intraday with our market directional lines:

GBPUSD:

Triggered long at A, hit first target at B, moved stop under UBreak and still holding second half. Note the Comber 13 sell signal right at the high:

Tradesight July 2013 Futures Results

Before we get to July’s numbers, here is a short reminder of the results from June. The full report from June can be found here. You can also go back indefinitely by clicking here and scrolling down.

Tradesight Tick Results for June 2013

Number of trades: 25

Number of losers: 7

Winning percentage: 68%

Net ticks: +30.5 ticks

Reminder: Here are the rules.

1) Totals for the month are based on trades that occurred on trading days in the calendar month.

2) Trades are based on the calls in the Messenger exactly as we call them and manage them and do not count everything you could have done from taking our courses and using our tools.

3) All trades are broken into two pieces, with the assumption that one half is sold at the first target and one half is sold at the final exit. These are then averaged. So if we made 6 ticks on one half and 12 on the second, that’s a 9-tick winner.

4) Pure losers (trades that just stop out) are considered 7 tick losers. We don’t risk more than that in the Messenger calls.

You can go through the reports and compare the breakdown that I give as each trade is reviewed.

Tradesight Tick Results for July 2013

Number of trades: 21

Number of losers: 7

Winning percentage: 66.7%

Net ticks: +34 ticks

Once again, we traded futures even less based on our recent assessment of the state of the various asset classes. There were several days either without calls, without a trigger, or with a call that we canceled because action was so light. There were even a couple of days that we closed out a trade near even when it just wasn't moving for too long.

Having said that, our desire to be picky seems to be working as we put together another decent month of gains on fewer trades.

There really isn't much else to say. We need bigger movement in the indices, which typically comes from volume, before we are going to step back into the Futures arena full throttle. But, we're doing OK but being picky.

Tradesight July 2013 Futures Results

Before we get to July’s numbers, here is a short reminder of the results from June. The full report from June can be found here. You can also go back indefinitely by clicking here and scrolling down.

Tradesight Tick Results for June 2013

Number of trades: 25

Number of losers: 7

Winning percentage: 68%

Net ticks: +30.5 ticks

Reminder: Here are the rules.

1) Totals for the month are based on trades that occurred on trading days in the calendar month.

2) Trades are based on the calls in the Messenger exactly as we call them and manage them and do not count everything you could have done from taking our courses and using our tools.

3) All trades are broken into two pieces, with the assumption that one half is sold at the first target and one half is sold at the final exit. These are then averaged. So if we made 6 ticks on one half and 12 on the second, that’s a 9-tick winner.

4) Pure losers (trades that just stop out) are considered 7 tick losers. We don’t risk more than that in the Messenger calls.

You can go through the reports and compare the breakdown that I give as each trade is reviewed.

Tradesight Tick Results for July 2013

Number of trades: 21

Number of losers: 7

Winning percentage: 66.7%

Net ticks: +34 ticks

Once again, we traded futures even less based on our recent assessment of the state of the various asset classes. There were several days either without calls, without a trigger, or with a call that we canceled because action was so light. There were even a couple of days that we closed out a trade near even when it just wasn't moving for too long.

Having said that, our desire to be picky seems to be working as we put together another decent month of gains on fewer trades.

There really isn't much else to say. We need bigger movement in the indices, which typically comes from volume, before we are going to step back into the Futures arena full throttle. But, we're doing OK but being picky.

Tradesight July 2013 Forex Results

Before we get to Joly’s numbers, here is a short reminder of the results from June. The full report from June can be found here and you can get the last several months in a row vertically by clicking here and scrolling down.

Tradesight Pip Results for June 2013

Number of trades: 21

Number of losers: 8

Winning percentage: 62%

Worst losing streak: 2 in a row

Net pips: +210

Reminder: Here are the rules.

1) Calls made in the calendar month count. In other words, a call made on August 31 that triggered the morning of September 1 is not part of September. Calls made on Thursday, September 30 that triggered between then and the morning of October 1 ARE part of September.

2) Trades that triggered before 8 pm EST / 5 pm PST (i.e. pre Asia) and NEVER gave you a chance to re-enter are NOT counted. Everything else is counted equally.

3) All trades are broken into two pieces, with the assumption that one half is sold at the first target and one half is sold at the final exit. These are then averaged. So if we made 40 pips on one half and 60 on the second, that’s a 50-pip winner. If we made 40 pips on one half, never adjusted our stop, and the second half stopped for the 25 pip loser, then that’s a 7 pip winner (15 divided by 2 is 7.5, and I rounded down).

4) Pure losers (trades that just stop out) are considered 25 pip losers. In some cases, this can be a few more or a few less, but it should average right in there, so instead of making it complicated, I count them as 25 pips.

5) Trade re-entries are valid if a trade stops except between 3 am EST and 9 am EST (when I’m sleeping). So in other words, even if you are awake in those hours and you could have re-entered, I’m only counting things that I would have done. This is important because otherwise the implication is that you need to be awake 24/6. Triggers that occur right on the Big Three news announcements each month don’t count as you shouldn’t have orders in that close at that time.

You can go through the reports and compare the breakdown that I give as each trade is reviewed.

Tradesight Pip Results for July 2013

Number of trades: 30

Number of losers: 13

Winning percentage: 56.7%

Worst losing streak: 3 in a row

Net pips: +135

The ranges died down again late in the month, but there was some action early. We usually look for a slowdown going into August, and we got it. Therefore, we have now adjusted our size down to half size moving forward as we anticipate the slow August season due to summer Holidays. We will adjust our size back up accordingly.

Note that the catalyst for lowering our size is to see a poor week play out, and we got that in the last week of July where we actually lost 25 pips, including 3 losers in a row (the only time in the month that happened) and it was the only week of the month with net losses.

Interestingly, the 6-month average daily ranges went UP in July, with the EURUSD going from 107 to 108 and the GBPUSD going from 116 to 121. This is more a result of poor ranges dropping off six months ago than increased ranges in July, however.

It is still possible for August to be a decent month in Forex. We have had good ones before. But, our experience tells us that when ranges lighten up and less people are trading, we lower our size and expectations and trade more cautiously.

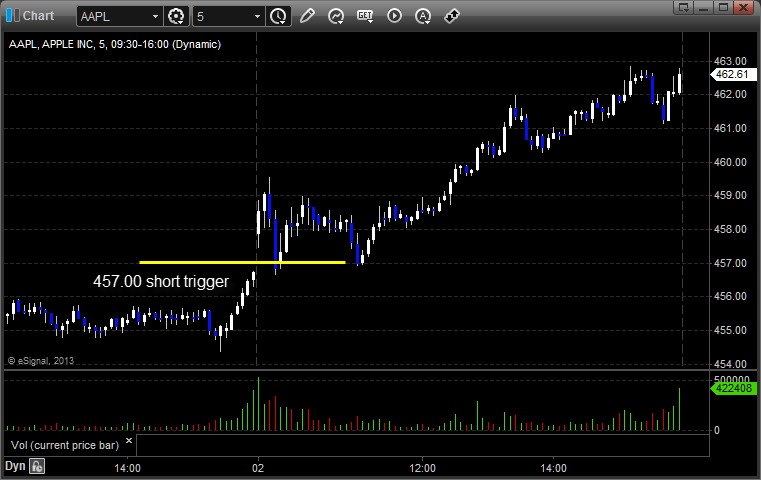

Stock Picks Recap for 8/2/13

With each stock's recap, we will include a (with market support) or (without market support) tag, designating whether the trade triggered with or without market directional support at the time. Anything in the first five minutes will be considered WITHOUT market support because market direction cannot be determined that early. ETF calls do not require market support, and are thus either winners or losers.

From the report, MDVN triggered long (with market support) and worked:

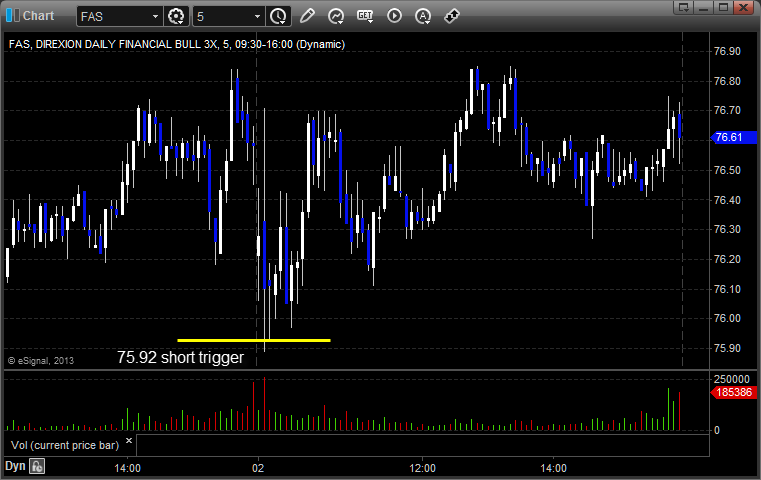

From the Messenger/Tradesight_st Twitter Feed, Rich's FAS triggered short (ETF, so no market support needed) and didn't work:

His AAPL triggered short (with market support) and didn't work:

His LNKD triggered short (without market support due to opening 5 minutes) and worked:

His GDX triggered long (ETF, so no market support needed) and didn't work:

TEVA triggered short (with market support) and didn't work:

Rich's HLF triggered short (with market support) and worked:

EBAY triggered long (with market support) and worked:

Rich's CLF triggered long (with market support) and worked:

In total, that's 8 trades triggering with market support, 4 of them worked, 4 did not.

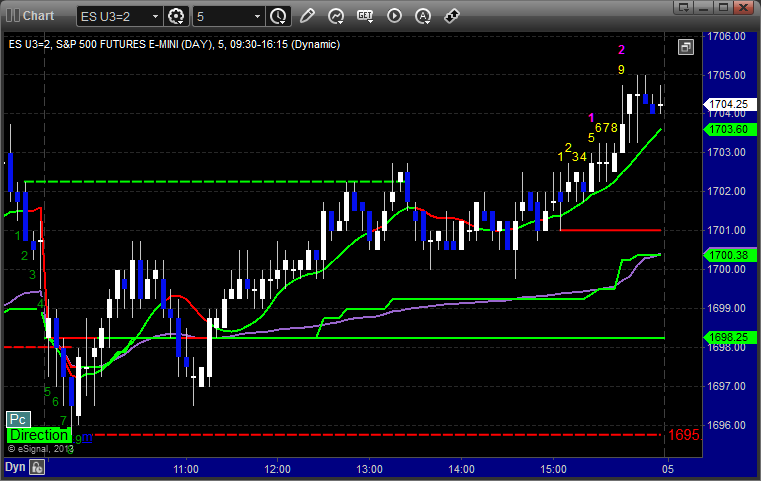

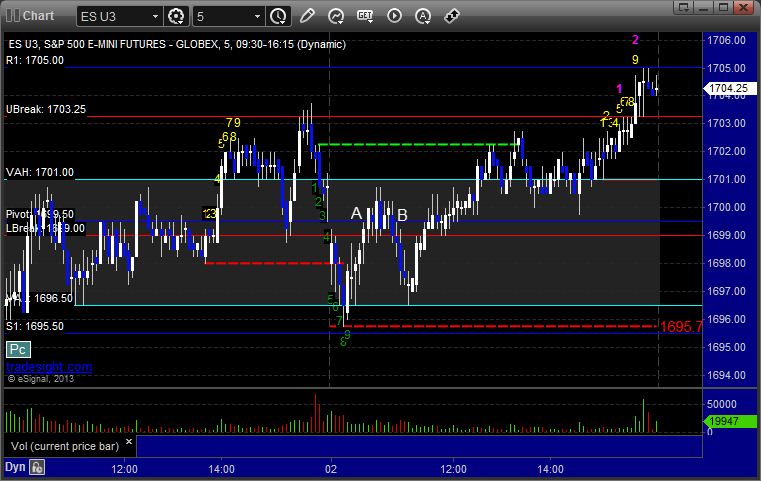

Futures Recap for 8/2/13

Two calls that triggered on the ES and NQ. See those sections below. Not much for results this week in a dull environment, and Friday wasn't great either. Volume hit 1.6 billion NASDAQ shares.

Net ticks: -7 ticks.

As usual, let's start by taking a look at the ES and NQ with our market directional lines, VWAP, and Comber on the 5-minute chart from today's session:

ES:

Mark's long triggered at A at 1699.75 and he finally closed it out even at B when nothing was happening:

NQ:

Just a reminder that we use half points for ticks on the NQ and not the quarter point measurement that the exchanges switched to in recent years. This allows us to use 6 ticks as a key target as we do on the other contracts. It also keeps the value of a tick at $10, closer to the value of a tick on the other contracts.

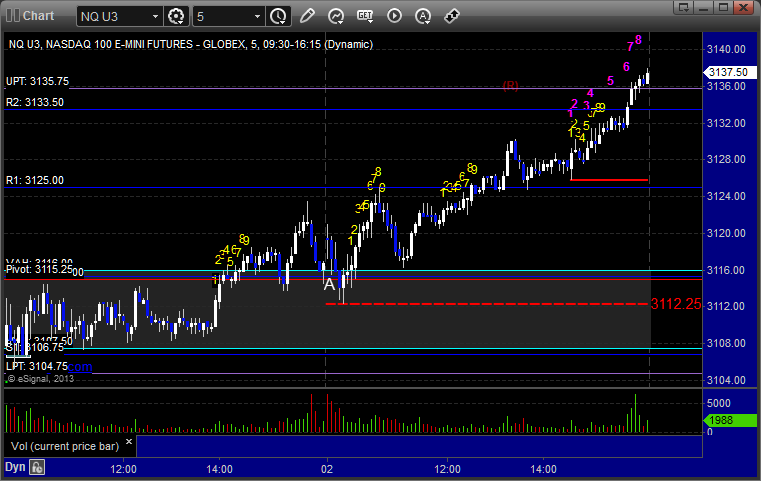

My call triggered short at A at 3114.50 and missed the first target by a tick, ended up stopping:

Futures Recap for 8/2/13

Two calls that triggered on the ES and NQ. See those sections below. Not much for results this week in a dull environment, and Friday wasn't great either. Volume hit 1.6 billion NASDAQ shares.

Net ticks: -7 ticks.

As usual, let's start by taking a look at the ES and NQ with our market directional lines, VWAP, and Comber on the 5-minute chart from today's session:

ES:

Mark's long triggered at A at 1699.75 and he finally closed it out even at B when nothing was happening:

NQ:

Just a reminder that we use half points for ticks on the NQ and not the quarter point measurement that the exchanges switched to in recent years. This allows us to use 6 ticks as a key target as we do on the other contracts. It also keeps the value of a tick at $10, closer to the value of a tick on the other contracts.

My call triggered short at A at 3114.50 and missed the first target by a tick, ended up stopping: