I wrapped up my vacation today, so no official calls, but there were nice setups on the ES and NQ that anyone who has taken the course should have taken, so I will outline those. Meanwhile, the markets gapped up, filled the gap, headed lower over lunch, then recovered to the VWAP area on 1.6 billion NASDAQ shares for quarterly contract roll.

Net ticks: +0 ticks.

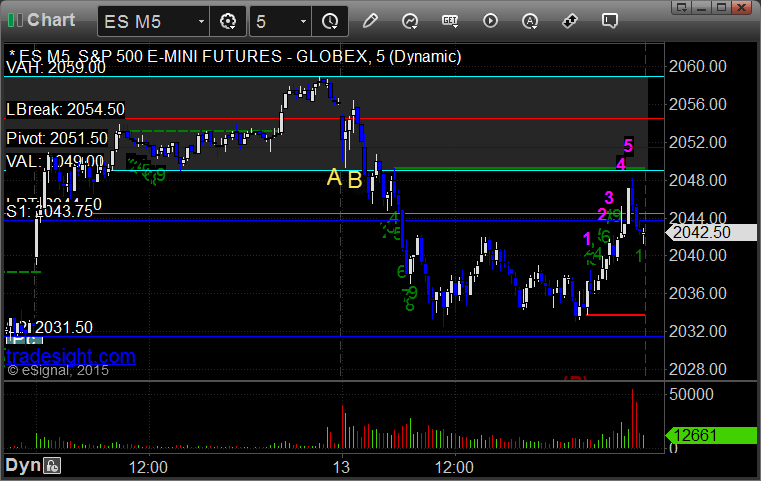

As usual, let’s start by taking a look at the ES and NQ with our market directional lines, VWAP, and Comber on the 5-minute chart from today’s session:

ES and NQ Opening and Institutional Range Plays:

ES Opening Range Play triggered long at A and didn’t work, triggered short at B but that was pretty late for an OR play:

NQ Opening Range Play triggered long at A and worked, triggered short at B but that was pretty late for an OR play:

ES Tradesight Institutional Range Play:

NQ Tradesight Institutional Range Play:

ES:

Note the set of the VAL Level in the opening bar at A, gave you a short entry breaking under it at B:

NQ:

Just a reminder that we use half points for ticks on the NQ and not the quarter point measurement that the exchanges switched to in recent years. This allows us to use 6 ticks as a key target as we do on the other contracts. It also keeps the value of a tick at $10, closer to the value of a tick on the other contracts.

Note the set of the group of levels at A that triggered short at B: